Car insurance is a major financial burden for many students juggling tuition, rent, books, and basic living expenses. The good news? There are smart, proven strategies students can use to significantly lower their car insurance premiums without compromising on coverage. By understanding how insurance works and taking advantage of discounts and programs designed specifically for younger drivers, students can save hundreds—or even thousands—of dollars a year.

This article is your complete guide to securing low-cost car insurance as a student. Whether you’re attending college full-time, commuting to campus, or living away from home, the tips and insights below will help you find the best deals, avoid hidden costs, and stay protected on the road—all while sticking to your budget.

Why Affordable Car Insurance Matters for Students

Students often fall into a high-risk category for insurers due to age, lack of driving history, and limited income. That’s why affordable coverage isn’t just nice to have—it’s essential. Here’s why:

- Limited Financial Flexibility: Most students work part-time or rely on loans. Expensive premiums can strain already tight budgets.

- High Risk Equals High Rates: Statistically, drivers under 25 are more likely to be involved in accidents, making insurers charge more.

- Mandatory Legal Requirement: Driving without insurance can lead to fines, license suspension, or even criminal charges.

- Impact on Academic Life: Without a car—or the means to insure it—students may struggle to attend classes, internships, or part-time jobs.

Getting affordable coverage means peace of mind, legal compliance, and the ability to stay mobile and independent throughout school.

The Hidden Costs of Not Shopping Around Early

Many students stick with their parents’ insurer or simply renew without comparing quotes. This can lead to missed opportunities and hidden expenses:

- Overpaying for Coverage You Don’t Use: Not all students need full coverage if they drive an older vehicle.

- Missing Student Discounts: Some companies only apply discounts if asked or if the student profile is updated.

- Failing to Leverage Good Driving Records: Even a clean record can go unnoticed if insurers aren’t informed.

- Automatic Renewals Without Adjustments: Each renewal is a chance to negotiate or switch—don’t let it pass.

A quick online comparison takes less than 30 minutes and can save you hundreds per year.

How the Right Coverage Can Boost Student Confidence

Affordable insurance isn’t just about saving money—it’s also about giving students the assurance they need to focus on school and life:

- Driving Without Fear: Knowing that accidents or thefts are covered lets students focus on the road, not the risks.

- Proof of Responsibility: Maintaining your own insurance policy is a milestone toward adulthood and financial independence.

- Better Credit & Insurance History: Building a solid record with your insurer can help with future loans, rentals, and even job applications.

- No Disruption to School or Work: A covered incident means fast recovery—essential when your time and schedule are tight.

When insurance is both affordable and reliable, students can drive smarter and with more peace of mind.

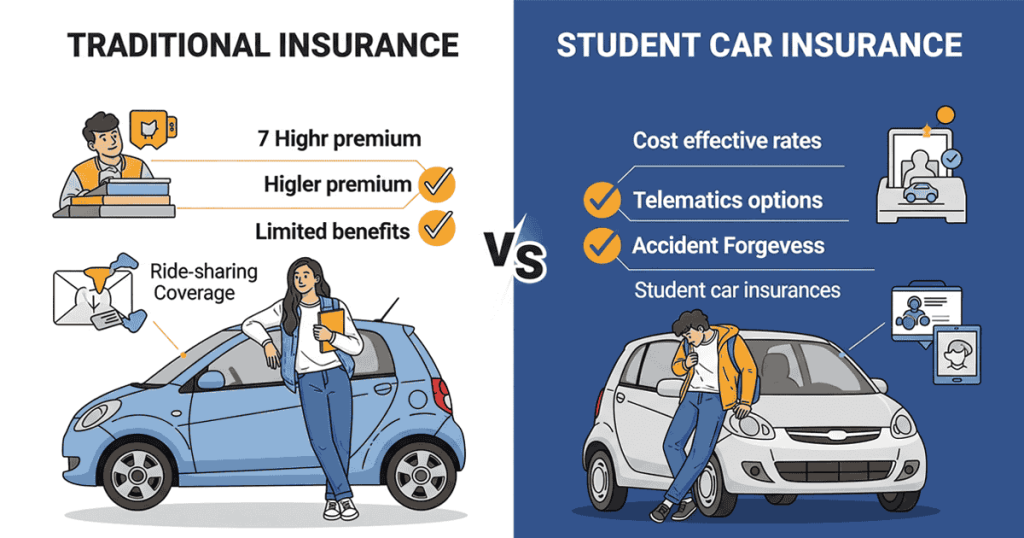

What Makes Student Car Insurance Different?

Student car insurance is tailored to drivers typically aged 18–25, many of whom are new to driving or lack significant credit history. These factors influence both pricing and eligibility for certain discounts. Here’s what makes it unique:

- Higher Base Rates: Younger drivers statistically cause more accidents, so premiums start higher.

- Flexible Coverage Options: Many insurers offer limited mileage or usage-based plans perfect for students who drive less.

- Discount-Oriented Policies: Good grades, safe driving apps, and distant student discounts make big savings possible.

- Parental Involvement: Students can often stay on family plans for reduced costs or be listed as secondary drivers.

Understanding these differences can help students choose policies that align with their actual needs—not just default settings.

How Age, School Status, and Driving History Affect Rates

Insurers use age and driving data to predict risk. Students should know how these factors work:

- Age: Premiums typically drop at age 25, but safe driving from 18–24 can still earn discounts.

- Enrollment Status: Full-time students are more likely to receive “good student” and “distant student” discounts.

- Driving Record: Clean records reduce costs, while violations (speeding, accidents) drive premiums up.

- Length of Insurance History: The longer you’ve been continuously insured, the better your rates.

Even a few months of good behavior can significantly reduce costs—so start early and drive safely.

The Role of Location and Vehicle Choice in Premiums

Where you live and what you drive both play major roles in how much you pay:

- Urban vs. Rural: Cities = higher rates due to more traffic and theft risk. Rural students usually pay less.

- Garaging Address: Living at school? Update your address for more accurate quotes.

- Vehicle Make/Model: Sports cars, luxury models, and high-performance vehicles cost more to insure.

- Safety Features: Anti-theft devices and safety ratings can bring premiums down.

Choose a car that’s cheap to repair, safe to drive, and low on the theft list for the best results.

Good Student Discounts: How to Qualify and Save

Insurers love responsible students—and they reward them. Here’s how to qualify for good student discounts:

- Minimum GPA Requirement: Most insurers require at least a B average (3.0 or higher).

- Proof of Enrollment: You’ll need a transcript, report card, or signed statement from your school.

- Full-Time Status: Discounts typically apply only to full-time students.

- Age Limits: Often capped at 25 years old.

Savings can range from 10% to 25%, depending on the insurer. If you’re excelling in class, make sure it reflects in your premium.

Why Usage-Based Insurance Is Perfect for Students

Usage-based insurance (UBI) uses mobile apps or plug-in devices to track real driving behavior. It rewards safe habits with lower rates:

- Monitors Speeding, Braking, and Mileage

- Great for Low-Mileage Students: If you don’t drive often, you’ll pay less.

- Instant Feedback: Apps help you become a safer driver.

- Major Insurers Offer It: Programs like Progressive’s Snapshot, Allstate’s Drivewise, and Root are popular.

UBI can save students 20–30% or more—especially if they drive less than 7,500 miles a year.

Bundling Insurance Policies: Worth It for Students?

Yes—if done right. Bundling refers to combining multiple insurance types (auto, renters, etc.) with one provider:

- Lower Premiums: Bundles often unlock 5–15% in savings.

- Simplified Payments: One bill, one account.

- Better Customer Service: Providers reward loyalty with smoother claims and discounts.

- Ideal for Dorm or Apartment Living: Renters insurance protects belongings and is often required.

If you rent near campus, bundling renters and auto can save both money and stress.

How One Student Cut Her Premium by 40%

Meet Jenna, a 20-year-old college junior in Michigan. She used to pay $220/month for car insurance. After doing research and calling three providers, she:

- Switched to usage-based insurance

- Submitted her GPA (3.7) to get a good student discount

- Reduced her mileage by biking to class 3 days a week

Her new monthly premium? $133. That’s a 40% reduction, and she now uses those savings toward textbooks and groceries. Real people are saving—so can you.

Parental Tips: Keeping Student Drivers Protected for Less

Parents play a huge role in helping students save on insurance. Here’s how:

- Keep Them on Your Policy: It’s often cheaper than a separate policy.

- Teach Safe Driving Habits Early: Fewer tickets = better rates.

- Help Compare Quotes: Use your credit and driving history for leverage.

- Consider a Shared Vehicle: Fewer vehicles insured = fewer premiums.

Informed parents make better choices for their students’ long-term financial health.

The True Cost of Ignoring Student-Specific Discounts

Skipping student discounts is like leaving money on the table. Here’s what it might cost:

- Missing Good Grade Savings: Up to $600/year lost.

- Ignoring Low-Mileage Credits: Another $200–$300 wasted.

- Sticking With the Wrong Carrier: Potentially $1,000+ in lost savings over a 4-year degree.

Discounts aren’t automatic, students (and parents) must ask and apply. It’s worth the effort.

How to Keep Premiums Low Year After Year

Getting a good rate is only step one. Here’s how to maintain low premiums:

- Avoid Tickets or Accidents: They stay on your record for years.

- Keep Your Grades Up: Maintain GPA for continued discounts.

- Track Mileage: Fewer miles = lower rates.

- Re-shop Annually: Don’t let loyalty cost you money.

- Don’t Let Coverage Lapse: Gaps in insurance lead to big price hikes.

Discipline now builds a history of savings that pays off well into adulthood.

What to Review Before Renewing as a Student Driver

Before auto-renewing your policy, evaluate:

- Coverage Needs: Still using the same car? Still living on campus?

- Available Discounts: Any new achievements or grades to report?

- New Providers or Offers: What else is out there?

- Payment Plans: Annual or semi-annual often saves over monthly.

Renewals are the perfect time to negotiate or switch.

Upgrading Your Policy After Graduation

Graduating? Congrats! But don’t forget to upgrade your insurance too:

- Update Employment Info: Full-time jobs improve your profile.

- Check Driving Habits: More commuting may require more coverage.

- Reevaluate Deductibles: Higher income = higher deductible = lower premium.

- Ask About Loyalty Upgrades: Many insurers reward long-term customers post-graduation.

Don’t just roll over your student plan—customize your coverage for adult life.

FAQs About Student Car Insurance

1. What is the cheapest car insurance option for students?

Generally, liability-only coverage with usage-based tracking is cheapest. Look for providers offering student-specific discounts.

2. Can I stay on my parent’s car insurance while in college?

Yes, if you live at home or drive a family car. It’s often cheaper than getting your own policy.

3. Do students really get discounts for good grades?

Absolutely. Most insurers offer 10–25% discounts for a GPA of 3.0 or higher.

4. How does location affect my student insurance rate?

Urban areas cost more due to theft and accidents. Rural or suburban areas tend to be cheaper.

5. Is usage-based insurance safe and reliable for students?

Yes. These programs are app-based, safe, and can dramatically reduce rates for safe drivers.

6. What should students look for in a low-cost policy?

Essential coverage (liability, maybe collision), high deductibles, and maximum discounts.

7. Does car type impact student insurance premiums?

Yes. Older, safer, fuel-efficient cars with low repair costs are cheaper to insure.

Final Thoughts

Car insurance doesn’t have to be a financial nightmare for students. With smart planning, safe driving, and a bit of research, students can secure low-cost, high-value coverage that supports them throughout college—and sets them up for financial success beyond graduation.