When you own an older car, finding the right insurance quote can be a bit tricky. With factors like age, condition, and mileage coming into play, it’s essential to know what you’re looking for when shopping for coverage. Whether you own a classic car or a daily driver, securing the best insurance rates is possible, but only if you understand what influences the premiums.

Older cars come with their unique set of advantages and challenges when it comes to car insurance. On one hand, the lower market value means you’re paying less for the actual vehicle itself, which can lead to lower insurance premiums. However, older cars can also present more risk for insurers, especially if the parts are harder to replace or repair. Understanding these dynamics can help you make informed decisions about the type of coverage you need and how to reduce your premiums.

Why Older Cars Are Cheaper to Insure: A Detailed Breakdown

Understanding the factors that make older cars cheaper to insure is key to saving money. Here’s a breakdown of why older cars can often mean lower insurance premiums:

- Lower Market Value: Since older cars tend to have a lower market value, the cost to repair or replace the vehicle in the event of an accident is reduced. Insurance companies take this into account when calculating premiums.

- Reduced Risk of Theft: Older cars tend to be less attractive to thieves compared to new, high-tech vehicles. This can lower your comprehensive insurance premiums.

- Lower Cost of Parts: Many older cars have parts that are more readily available and less expensive to replace. This can mean fewer claims for insurance companies, which may result in lower rates.

- Simple Design: Older vehicles typically lack complex electronics and advanced safety features. While this may be a disadvantage in some ways, it also makes them less expensive to repair and insure.

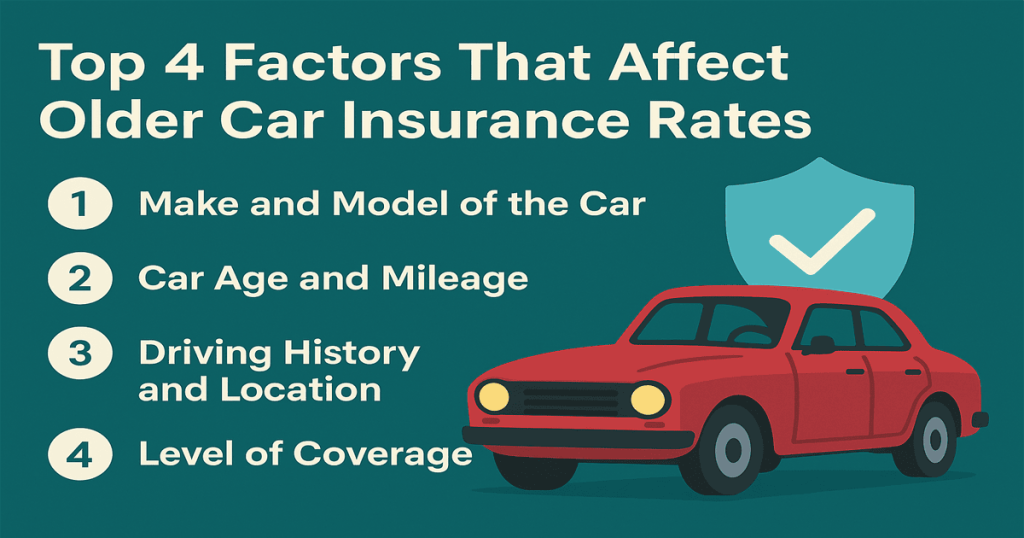

Top 4 Factors That Affect Older Car Insurance Rates

When you’re shopping for insurance quotes for older cars, several important factors influence the final premium. Let’s take a deeper look at the top factors that can impact how much you pay for coverage:

- Make and Model of the Car

The specific make and model of your car can significantly influence your insurance quote. Cars that are harder to repair, or have higher performance engines, often carry higher premiums due to the higher cost of repairs and potential for accidents. - Car Age and Mileage

Naturally, the older the car, the more likely it is to require repairs. Cars with high mileage may also present a higher risk for insurers due to wear and tear, leading to higher premiums. - Driving History and Location

A clean driving record is one of the best ways to secure lower insurance rates. Additionally, where you live matters. Urban areas with higher traffic and accident rates may drive up premiums, while rural areas might offer more affordable options. - Level of Coverage

If you opt for full coverage, including comprehensive and collision insurance, expect to pay more. On the other hand, liability insurance alone can significantly lower premiums for older vehicles.

Is Classic Car Insurance Worth It for Your Vintage Ride?

If you own a vintage or classic car, you may be wondering if classic car insurance is worth it. Classic car insurance is tailored for vehicles that are over a certain age, typically 20 years or older, and are often rare or limited-production models. Here’s what you need to know:

- Specialized Coverage: Classic car insurance typically provides more specialized coverage than standard auto insurance policies. This is essential for cars that may be difficult or costly to replace or repair.

- Guaranteed Value: Many classic car policies offer a guaranteed value option, which means that in the event of a total loss, you’ll be reimbursed for the car’s value at the time the policy was written, rather than the depreciated value.

- Lower Premiums for Low Mileage: Many classic cars are driven only occasionally, which can significantly reduce premiums. These cars are often seen as lower risk due to the limited mileage and reduced exposure to accidents.

Understanding the Pros and Cons of Insuring an Older Car

There are various benefits and drawbacks when insuring older cars, and it’s essential to weigh these when selecting a policy:

Pros:

- Cost Savings on Premiums: As mentioned earlier, older cars generally cost less to insure, especially if they have lower market value and are less expensive to repair.

- Availability of Discounts: Older car owners might qualify for additional discounts based on their driving habits, location, and lack of accidents over the years.

- Simplicity of Coverage: Older cars often don’t require advanced coverage types. For example, you may not need comprehensive or collision insurance if your car is already paid off and has a low market value.

Cons:

- Higher Repair Costs: Older cars might have parts that are no longer being manufactured, making repairs more expensive and harder to come by. This can increase the likelihood of filing claims.

- Limited Safety Features: Many older cars lack modern safety features like airbags, anti-lock brakes, and traction control, which can increase premiums.

- Outdated Technology: Without modern technology, older cars are more susceptible to breakdowns, which can raise your risk profile for insurers.

How Car Age Affects Insurance Premiums and Coverage?

The age of your car is one of the primary factors that affect the insurance quote you receive. When your car ages, it experiences natural wear and tear, and it becomes less reliable. This is why many insurers adjust premiums based on age and condition.

- Insurance for Cars Older Than 10 Years: Cars over 10 years old are often eligible for lower premiums since the car’s value has significantly decreased.

- Cars Between 5-10 Years Old: This range can see moderate premiums, depending on the model and condition of the vehicle.

- Cars Under 5 Years Old: These vehicles tend to have higher premiums, as their market value is still high, and the cost of repairs or replacement can be expensive.

The Best Insurance Companies for Classic Car Owners in 2025

If you’re an owner of a classic or vintage car, there are several insurance companies that specialize in providing coverage for older cars. Here are some of the best companies to consider:

- Hagerty Insurance: One of the most trusted names in classic car insurance, offering comprehensive coverage options that include agreed value, roadside assistance, and more.

- American Collectors Insurance: Specializing in classic cars and offering flexible policies that can be tailored to your specific needs, American Collectors Insurance is a solid option for those with rare or vintage cars.

- Grundy Insurance: Known for providing guaranteed value coverage for older vehicles, Grundy is a favorite among classic car owners looking for specialized policies.

Common Mistakes When Insuring Older Cars and How to Avoid Them

While insuring an older car may seem straightforward, there are common mistakes people often make when choosing a policy. These mistakes can cost you in the long run, so it’s essential to avoid them.

- Not Choosing the Right Coverage

Many older car owners opt for minimum coverage, not realizing that they may need additional protection for repairs or accidents. A comprehensive policy ensures you’re fully covered in case of an accident. - Ignoring the Car’s Value

When purchasing insurance for older cars, make sure you take the car’s true market value into account. Don’t assume that the standard policy will automatically cover the full replacement cost. - Underestimating Liability

Older cars can still cause significant damage in an accident, so it’s essential to have adequate liability coverage. Don’t skimp on liability insurance to save money.

How to Compare Insurance Quotes for Older Cars Quickly?

When comparing insurance quotes for older cars, it’s essential to understand how different factors impact premiums. Here are some steps to ensure you get the best deal:

- Check Multiple Providers: Use online comparison tools to get quotes from multiple insurance companies, allowing you to compare coverage, premiums, and discounts.

- Review Coverage Options: Make sure you understand the different types of coverage available for older cars, including liability, comprehensive, and collision insurance.

- Ask About Discounts: Some insurers offer discounts for things like low mileage, safe driving, and multi-policy discounts. Make sure to inquire about these potential savings.

The Cost-Saving Benefits of Insuring Your Older Car

There are several cost-saving benefits associated with insuring an older vehicle. By understanding how your older car impacts your insurance rates, you can make decisions that help keep premiums low:

- Low Market Value: Older cars usually have a lower market value, which means that insurance companies will typically charge less to cover them.

- No Loan Payments: If you own your older car outright, you don’t have to pay for the high premiums associated with new cars, which are often financed.

- More Discount Opportunities: Insurers offer discounts for things like low mileage, good driving records, and safety features. These discounts can significantly lower your premium.

What to Look for in an Older Car Insurance Policy?

When shopping for insurance for older cars, here’s what to look for in your policy:

- Guaranteed Value Coverage: This type of coverage ensures that in the event of a total loss, you’re reimbursed for the car’s agreed value, not its depreciated market value.

- Low Deductibles: Opt for a policy that allows you to choose low deductibles to reduce your out-of-pocket costs in the event of a claim.

- Roadside Assistance: Consider adding roadside assistance to your policy, especially if your older car is prone to breakdowns.

Is It Better to Choose Full Coverage or Liability for Your Older Car?

Deciding between full coverage and liability coverage depends on the condition and value of your older car. If your car is still worth a significant amount, full coverage may be the better option to protect your investment. However, if your car is worth less and you can afford to replace it, liability coverage might be sufficient.

How to Get Discounts on Older Car Insurance Policies?

Many insurance companies offer discounts for older cars based on their lower risk profile. Here are some discounts to ask about:

- Low Mileage Discounts: If you don’t drive your older car much, you may qualify for a low mileage discount.

- Safety Feature Discounts: If your older car has safety features like airbags or anti-lock brakes, you may be eligible for discounts.

- Multi-Policy Discounts: If you have other insurance policies with the same provider, you may receive a discount for bundling.

When Is It Time to Consider Letting Go of Your Older Car Insurance?

It may be time to reconsider your older car insurance policy if your vehicle has become too expensive to maintain, or if it no longer holds enough value to justify the insurance cost. If the premiums exceed the value of the car, it might be time to reconsider your options or even drop coverage altogether.

FAQ

Do older cars really cost less to insure than newer ones?

Yes, older cars tend to cost less to insure due to their lower market value, reduced theft risk, and lower repair costs. However, the savings depend on the car’s condition, make, model, and coverage options.

What are the best types of insurance for classic and vintage cars?

The best insurance for classic cars typically includes agreed-value coverage, which guarantees a specific payout in the event of a loss, and specialized protection for rare or collectible cars.

How can I find the cheapest insurance for my older car in 2025?

To find the cheapest insurance for your older car, compare quotes from multiple providers, consider increasing your deductible, and ask about discounts for low mileage or safe driving.